Health Insurance in America: The States Facing the Highest Coverage Gaps and Rising Costs

Key highlights

- Florida ranks as the most stressed state for health insurance, with a score of 8.73 out of 10.

- Texas has the highest uninsured rate in the U.S., with over one in six (16.7%) residents lacking coverage.

- Idaho records the highest health insurance search demand, with 1,161 searches per 100,000 people.

- Hawaii has seen the largest increase in premiums over the past decade, rising by half (50.2%).

- On average, health insurance premiums have increased by over a third (35.8%) nationwide over the last 10 years.

In the past month alone, more than 1.2 million Americans have searched for health insurance coverage, highlighting how frequently affordability and access are on Americans’ minds.

Nationally, 7.6% of residents remain uninsured, while employees contribute an average of $6,927 per year toward employer-sponsored family coverage. Over the past decade, that cost has risen by 35.8%, reflecting the growing financial burden associated with maintaining health insurance.

However, new data shows that this burden is not spread evenly. Some states face significantly higher uninsured rates, rapidly rising premiums, and far greater search demand, pointing to clear geographic differences in both access and affordability.

To understand where Americans are most affected, this study analyzes insurance coverage levels, long-term premium trends, and search behavior across every state, revealing where pressure is highest, where costs are rising fastest, and where demand for insurance is growing most quickly.

Access to healthcare plays a key role in managing long-term conditions

Health insurance plays a central role in determining access to treatment, particularly for chronic conditions such as obesity and diabetes.

More than two in five U.S. adults are classified as obese, increasing the risk of serious long-term complications.1 Treatments such as compounded tirzepatide and being able to buy semaglutide online are increasingly used to support weight loss as part of a wider approach to improving health outcomes.

However, access to these treatments often depends on insurance coverage. Without it, affordability can become a significant barrier, particularly as demand continues to rise.

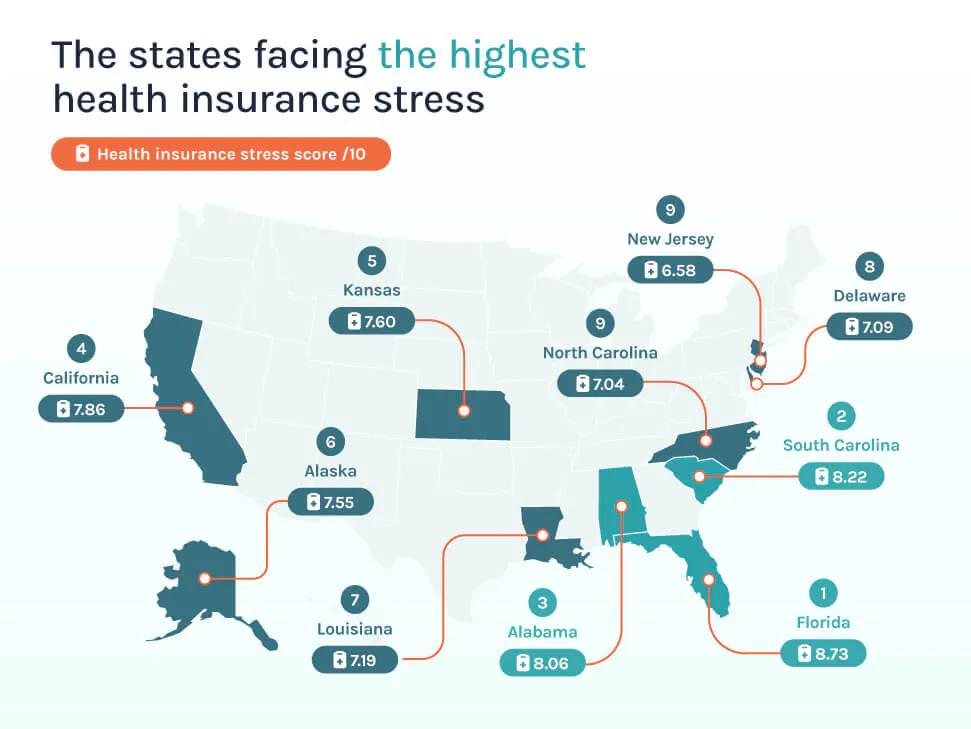

The states facing the highest health insurance stress

Health insurance challenges vary sharply across the United States, but some states consistently rank poorly across multiple measures, including coverage gaps, rising premiums, and search demand.

By combining these factors into an overall ‘insurance stress score,’ it is clear where residents are facing the most pressure.

| Rank | State | Residents without health insurance | Average annual employee contribution* | 10-year change in average annual employee contribution* | Health insurance plan searches per 100,000 people | Health insurance stress score /10 |

|---|---|---|---|---|---|---|

| 1 | Florida | 10.9% | $8,831 | 40.9% | 913 | 8.73 |

| 2 | South Carolina | 9.0% | $7,832 | 47.5% | 330 | 8.22 |

| 3 | Alabama | 8.2% | $7,808 | 45.2% | 666 | 8.06 |

| 4 | California | 5.9% | $9,148 | 45.8% | 685 | 7.86 |

| 5 | Kansas | 8.5% | $7,207 | 43.0% | 616 | 7.60 |

| 6 | Alaska | 11.0% | $8,409 | 49.7% | 56 | 7.55 |

| 7 | Louisiana | 7.7% | $8,600 | 41.2% | 246 | 7.19 |

| 8 | Delaware | 6.9% | $7,726 | 45.5% | 297 | 7.09 |

| 9 | North Carolina | 8.6% | $7,968 | 41.7% | 97 | 7.04 |

| 10 | New Jersey | 7.7% | $7,305 | 41.0% | 280 | 6.58 |

*Employer-sponsored family coverage

1. Florida named America’s most stressed state for health insurance, with 1 in 10 residents uninsured

Florida records the highest overall insurance stress score in the country at 8.73 out of 10.

Demand for coverage is among the highest in the U.S. Florida records 913 health insurance-related searches per 100,000 people, more than three times the national average of 251. This suggests that many residents are actively seeking alternative plans or more affordable options.

The state has an uninsured rate of over 1 in 10 (10.9%), significantly above the national average of 7.6%. At the same time, employees contribute an average of $8,831 per year towards family coverage, placing Florida among the most expensive states for employer-sponsored insurance.

Premiums have also risen sharply, increasing by over two-fifths (40.9%) over the past decade. Taken together, these factors highlight a combination of high costs, limited coverage, and sustained demand, all of which contribute to Florida’s top ranking.

2. South Carolina is among the top states for health insurance stress, with insurance premiums increasing by almost half in 10 years

South Carolina ranks second overall, with a health insurance stress score of 8.22.

Over the past 10 years, premiums in the state have increased by almost half (47.5%), one of the fastest rates of growth nationwide. On top of this, 9.0% of residents are uninsured, while the average annual employee contribution stands at $7,832.

Search demand remains elevated at 330 searches per 100,000 people, above the national average. This indicates consistent interest in finding coverage, likely driven by rising costs and affordability pressures.

Although South Carolina does not have the highest uninsured rate, the combination of rapid premium growth and sustained search demand suggests that access to affordable insurance is becoming challenging.

3. Alabama ranks third for health insurance stress, with 666 health insurance searches per 1,000 people

Alabama ranks third, with an overall score of 8.06. Search demand is significantly higher than the national average. Alabama records 666 searches per 100,000 people, more than double the U.S. benchmark, indicating that many residents are actively exploring insurance options.

The state has an uninsured rate of 8.2%, slightly above the national average of 7.6%, while employees contribute an average of $7,808 annually towards family coverage. Premiums have risen by 45.2% over the past decade, placing additional strain on households.

This strain intensified in 2026 following the expiration of enhanced federal tax credits. Alabama Arise reported that marketplace premiums for some residents have nearly doubled, with roughly 130,000 Alabamians at risk of losing coverage due to these soaring costs.²

What the experts say…

Rob Stransky, President at NiceRx, says:

“Health insurance plays a critical role in shaping both financial security and access to care across the United States. As premiums rise and coverage gaps persist in some states, many people are left to make complex decisions about their healthcare.

“For individuals managing long-term conditions such as obesity, access to treatment can be challenging without adequate insurance. Medications such as GLP-1s are increasingly used to support weight loss and improve long-term health outcomes, but cost remains a key barrier.

“While insurance can help reduce these costs, alternative pathways are becoming more common. Clinically guided services, including access to treatments such as compounded tirzepatide or the ability to buy semaglutide online, may help some patients access treatment more affordably when used alongside appropriate medical support.

“Alongside this, comparing providers, exploring different pricing models, and seeking clinically supervised options can help individuals reduce costs and improve access, even without traditional insurance coverage.”

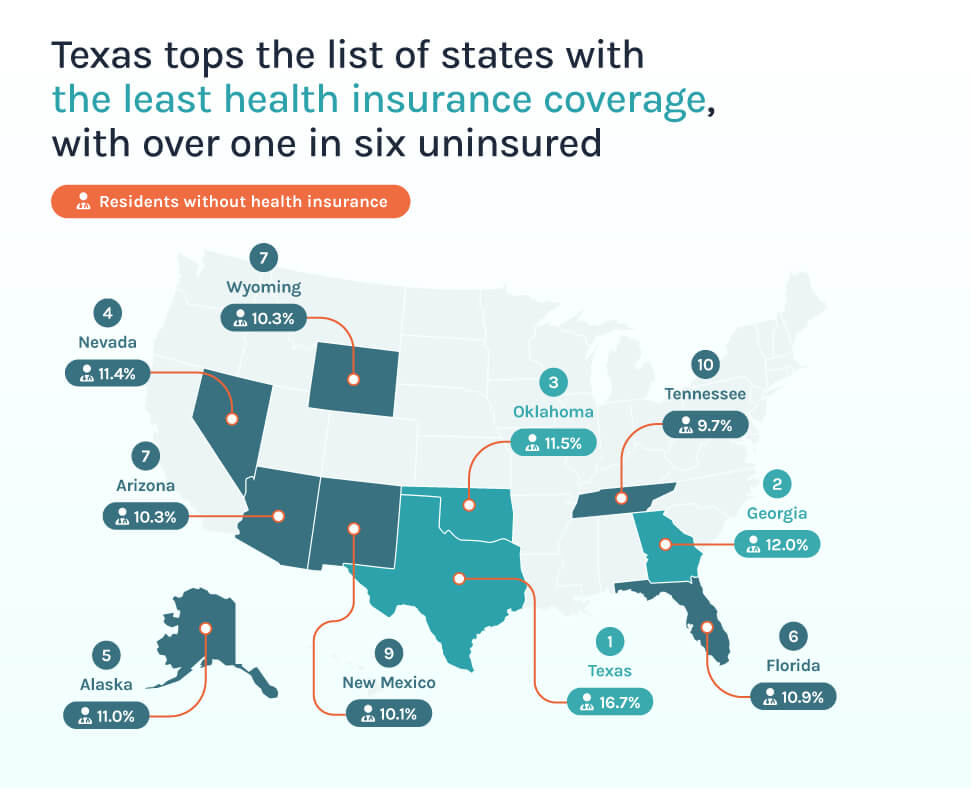

Texas tops the list of states with the least health insurance coverage, with over one in six uninsured

Health insurance coverage varies widely, with some states reporting uninsured rates more than double the national average of 7.6%.

| Rank | State | Residents without health insurance |

|---|---|---|

| 1 | Texas | 16.7% |

| 2 | Georgia | 12.0% |

| 3 | Oklahoma | 11.5% |

| 4 | Nevada | 11.4% |

| 5 | Alaska | 11.0% |

| 6 | Florida | 10.9% |

| 7 | Arizona | 10.3% |

| 7 | Wyoming | 10.3% |

| 9 | New Mexico | 10.1% |

| 10 | Tennessee | 9.7% |

At the top of the rankings, Texas stands out, with 16.7% of residents lacking health insurance. Because Texas has not expanded Medicaid, over 720,000 uninsured adults in working, low-wage families fall into a coverage gap, unable to access affordable Marketplace subsidies.³

Other Southern states also feature prominently, with Georgia (12.0%), Oklahoma (11.5%), and Florida (10.9%) all recording elevated uninsured populations. Analysis from the Kaiser Family Foundation indicates that these coverage gaps are driven by factors such as affordability and the lack of employer-sponsored insurance, particularly in states that have not expanded Medicaid.⁴

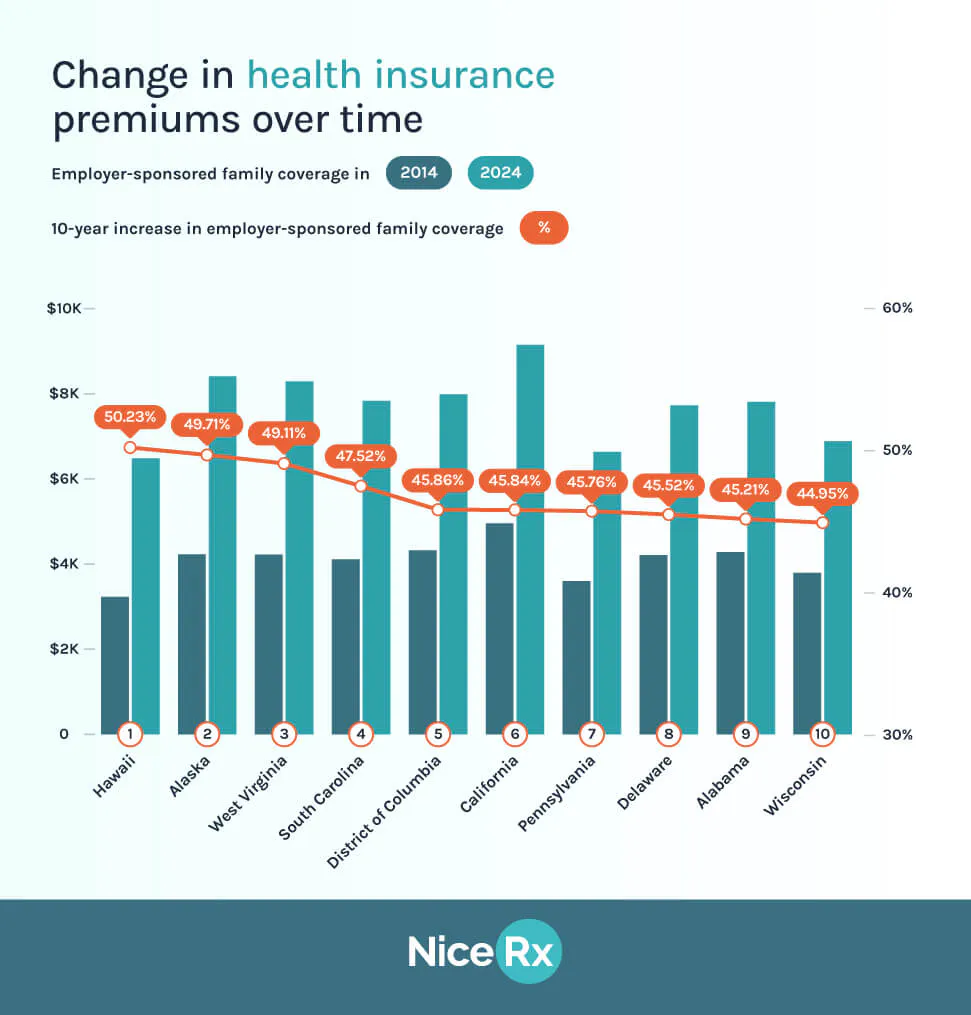

Change in health insurance premiums over time

Over the past decade, employer-sponsored family health insurance costs have risen sharply across every U.S. state, with increases ranging from under 20% to more than 50%. While the national trend shows sustained upward pressure on premiums, the data reveals clear regional variation in how quickly costs have accelerated.

| Rank | State | Employer-sponsored family coverage in 2014 | Employer-sponsored family coverage in 2024 | 10-year increase in employer-sponsored family coverage |

|---|---|---|---|---|

| 1 | Hawaii | $3,227 | $6,484 | 50.23% |

| 2 | Alaska | $4,229 | $8,409 | 49.71% |

| 3 | West Virginia | $4,219 | $8,290 | 49.11% |

| 4 | South Carolina | $4,110 | $7,832 | 47.52% |

| 5 | District of Columbia | $4,324 | $7,987 | 45.86% |

| 6 | California | $4,955 | $9,148 | 45.84% |

| 7 | Pennsylvania | $3,598 | $6,633 | 45.76% |

| 8 | Delaware | $4,209 | $7,726 | 45.52% |

| 9 | Alabama | $4,278 | $7,808 | 45.21% |

| 10 | Wisconsin | $3,791 | $6,886 | 44.95% |

At the top of the range, Hawaii has seen the steepest increase, with employer-sponsored family coverage rising by just over 50% since 2014. Alaska (49.7%) and West Virginia (49.1%) follow closely behind, all three reflecting a broader pattern seen in healthcare affordability research that smaller or more geographically challenging states tend to face higher per-capita cost growth due to delivery constraints and limited provider networks.⁵

States including South Carolina (47.5%), California (45.8%), Pennsylvania (45.8%), and Alabama (45.2%) also sit well above the national growth trajectory. This suggests that rising employer healthcare costs are not confined to rural or remote systems. The Commonwealth Fund has previously noted that employer premiums have steadily outpaced wage growth across all income groups over the last decade, contributing to growing affordability strain even among insured households.⁶

Health insurance demand is rising sharply in some states

Search behavior provides additional insight into how Americans are responding to rising healthcare costs.

While the national average is 251 searches per 100,000 people, several states note significantly higher levels of demand.

Idaho stands out, with 1,161 searches per 100,000 people, more than four times the national average. While it is a smaller state, this spike is better understood in the context of recent coverage disruptions, with reporting indicating that the end of enhanced federal subsidies could leave around 30,000 Idahoans newly uninsured, putting strong focus on affordability and plan access in the state.⁷

Illinois (1,085) and Michigan (898) also rank among the highest. In many cases, higher search demand aligns with rising premiums, coverage gaps, or both. This can be seen in Texas, where the uninsured rate reaches 16.7%, the highest in the country, alongside high insurance search activity. Florida also shows a similar dynamic, combining a 10.9% uninsured rate with some of the highest search volumes nationally (913 per 100,000), suggesting active consumer engagement in a high-cost, high-coverage-gap environment.

This suggests that as affordability pressures increase, more residents are actively seeking alternative insurance options or exploring ways to reduce healthcare costs.

How to access GLP-1 treatments without insurance

For individuals without health insurance, accessing treatments such as GLP-1 medications can be challenging, particularly as demand continues to increase.

However, there are several ways to improve affordability and access:

1. Explore patient assistance programs where eligible

If you are without health insurance, manufacturer support programs may help reduce costs. Novo Nordisk offers a patient assistance program (PAP) that can provide free medications such as Ozempic and Rybelsus to you if you meet specific income and insurance criteria. Eligibility typically depends on household income, residency status, and lack of participation in government insurance programs.

Savings card schemes may also be available if you’re commercially insured, offering reduced-cost access to certain medications, subject to coverage and eligibility.

2. Use prescription discount services to reduce retail costs

Prescription discount platforms such as GoodRx, SingleCare, WellRx, and Optum Perks may offer reduced pricing at participating pharmacies. These services can provide savings of up to 27% off retail prices, depending on location, dosage, and pharmacy availability.

While savings vary, these tools can help reduce out-of-pocket costs if you are not eligible for manufacturer assistance programs.

3. Check eligibility for public support programs

Some government-backed schemes may reduce costs if you’re eligible. Medicare Part D Extra Help is designed to help you with prescription costs if you are on a low income, though coverage for weight-loss indications is limited.

In most cases, GLP-1 medications such as semaglutide are only covered under Medicare or Medicaid when prescribed for type 2 diabetes, rather than weight management.

4. Consider clinically guided compounded alternatives

In some cases, compounded semaglutide may be prescribed when personalized dosing or alternative formulations are required. While it contains the same active ingredient, it is not FDA-approved and is typically used when branded medications are inaccessible due to cost or supply constraints.

When clinically appropriate, compounded options may offer a lower-cost alternative to branded GLP-1 medications, though suitability depends on individual medical assessment.

5. Use telehealth services for faster access and assessment

Telehealth consultations allow patients to be assessed remotely by licensed clinicians, often reducing the need for in-person appointments. After clinical review, a prescription may be issued, with medication delivered directly to the patient in some cases.

This approach can improve access if you are facing time, location, or affordability barriers, while still ensuring medical oversight.

6. Always ensure prescriptions come from licensed providers

Regardless of the access route, GLP-1 medications should be obtained only from licensed healthcare professionals and regulated pharmacies. This helps ensure safety, appropriate dosing, and product authenticity.

You should avoid unverified online sources, as medication quality and legitimacy can vary significantly outside regulated supply chains.

Methodology

NiceRx is a telehealth company that helps patients access prescription treatments and clinically guided support through a fully online service.

With more than 1.2 million monthly searches related to health insurance, understanding where coverage gaps, rising costs, and demand are most pronounced can help highlight where support may be needed most.

To explore these trends, we analyzed data across all 50 U.S. states using the following factors:

- Percentage of residents without health insurance, sourced from the U.S. Census Bureau

- Average annual employee contribution for family coverage, based on employer-sponsored health insurance data sourced from KFF.

- 10-year percentage change in premiums, calculated using historical data on employee contributions.

- Search interest, based on Google Keyword Planner data for “health insurance plans,” normalized per 100,000 people.

Each state was ranked across these factors and combined into a normalized score out of 10 to create an overall ‘health insurance stress score.’